Global energy disruptions are rising. Conflicts drive these disruptions. The Russia-Ukraine war is one conflict. Iran-US tensions are another. These are not temporary problems. These are structural shifts.

Strategic chokepoints amplify risks. The Strait of Hormuz is critical. Disruption there affects everything. Supply routes matter. Control matters more in such cases. Hence, the energy crisis is becoming a real issue.

India faces vulnerability. India is a major energy importer. This creates macroeconomic exposure. The economy is sensitive. Oil prices matter deeply. The energy crisis is a real issue.

India’s Structural Energy Vulnerability

India imports crude oil. The percentage is high. Around eighty-five percent is imported. Domestic reserves are limited. Refining dependency exists.

This creates exposure. Global volatility affects India directly. Price shocks translate immediately. The vulnerability extends beyond energy. Inflation is impacted. Fiscal balance suffers. Currency stability weakens.

The numbers are stark. The dependency is real. The risks are mounting.

Pressure on the Indian Rupee and the External Sector

Capital outflows are happening. Portfolio outflows reached eleven points eight billion in 2025. Four billion has flowed out in 2026 already. The trend continues.

Rupee depreciation is visible. The currency crossed ninety rupees per dollar. It moved to ninety-two. The slide is steady.

If oil prices rise sharply, consequences follow. Trade deficit expands significantly. Current Account Deficit may exceed sustainable levels. Three percent of GDP is considered sustainable. Breaching this creates problems.

Historical patterns exist. High oil prices lead to currency depreciation. Currency depreciation leads to imported inflation. The cycle is vicious. The damage is real.

| Period | Oil Price ($/barrel) | Rupee Value (₹/$) | CAD (% of GDP) | Key Notes |

| 2020-21 | $40-50 | ₹73-75 | -0.9% | Low global demand post-pandemic stabilized imports. business-standard |

| 2022-23 | $90-110 | ₹79-83 | -2.0% | Geopolitical shocks widened the trade deficit. fortune India |

| 2025 (Current) | $100-104 | ₹92 | -1.5% | Oil surge pressures rupee; services surplus offsets CAD. whalesbook+1 |

| Projected (High Oil) | $115+ | ₹95+ | 3%+ | $10/barrel rise adds 0.3-0.5% to CAD via import bill. multibagg+1 |

Threat to India’s “Goldilocks Phase”

Recent macro stability was remarkable. High growth existed. Seven to eight percent growth was achieved. Inflation remained low. Around two-point seven five percent was maintained.

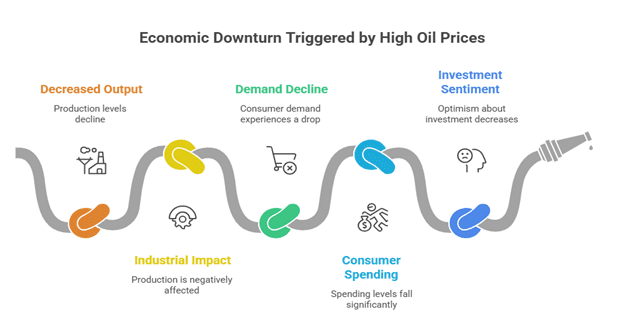

This was India’s Goldilocks phase. Not too hot. Not too cold. Just right. Energy crisis disrupt this balance.

Rising fuel costs create inflationary pressure. This pressure is upward. This pressure is persistent. Reduced consumption slows growth. The balance breaks. The stability ends.

Inflationary Pressures and Domestic Impact

Direct effects are immediate. LPG prices hike. Fuel shortages occur. Supply prioritization happens. Households feel the impact. Businesses adjust costs.

Indirect effects spread widely. Transportation costs are rising. Production costs have increased. Everything becomes expensive. The ripple effect is massive.

Estimates suggest outcomes. Inflation could exceed five percent. This happens if crude crosses one hundred dollars per barrel. Cost-push inflation becomes dominant. Demand-pull factors fade. Supply-side pressures take over.

Growth Outlook and Economic Slowdown Risks

RBI projects growth. Six point nine to seven percent is expected. This is a baseline projection. Downside risks exist.

Global uncertainty adds pressure. Capital flows reverse. Foreign investment hesitates. Growth momentum slows. The optimism fades.

Fiscal Stress and Policy Trade-offs

The government faces a dilemma. Two options exist. Neither is attractive.

- Option one is increasing fuel prices. This controls the fiscal burden. But inflation risk rises. Public discontent grows. Political costs mount.

- Option two is absorbing costs. Fiscal burden increases. Subsidies expand. Revenue losses accumulate. Deficit widens.

Fiscal indicators face pressure. The fiscal deficit target is four-point-three percent. Rising subsidies threaten this. Fertilizer subsidies are growing. Fuel subsidies are expanding. Excise duty cuts reduce revenue. Two rupee cut costs thirty-two thousand crore.

The choices are hard. The consequences are certain.

Strategic and Policy Responses

The strategic and policy responses are mentioned below:

- Short-term responses exist. The Economic Stabilization Fund was created by the government. One lakh crore is allocated to this fund. Strategic petroleum reserves are tapped. Buffer stocks are released as and when required.

- Medium-term measures are planned. Oil import sources are diversified from different countries. Dependence on single sources is reduced. Rupee stability measures strengthen. Currency management improves gradually.

- Long-term vision is clear. Renewable energy transition accelerates. Electric mobility gets pushed. Energy self-reliance is pursued. Atmanirbhar Bharat extends to energy. The strategy is comprehensive.

Way Forward: Building Economic Resilience

Import dependence must be reduced. This reduction is critical. This reduction is strategic. Energy diplomacy must be strengthened. Relationships matter. Sourcing options matter more.

Macroeconomic buffers need enhancement. Forex reserves must grow. Fiscal discipline must persist. Balancing act continues.

Growth-inflation trade-offs need calibration. Policy must be nuanced. Policy must be adaptive. The margin for error is small.

Conclusion

Global energy crisis are not temporary. These are not passing disruptions. These are structural risks. These are permanent features. The geopolitical landscape has changed. Energy has become weaponized.

India’s economic stability depends on responses. How effectively does India transition? Can vulnerability become resilience? The answer determines the future.

The evolving geopolitical landscape demands action. This action must be proactive. This action must be multi-dimensional. Policy must respond. Strategy must evolve. India must adapt.t

Very informative content….hatts off!!

Thank you, Prashant.

Pingback: Rupee Falling Amid Global War: RBI Faces Tough Choice Between Forex Reserves and Currency Stability - upscpscpedia.com